It allows a trustee or successor trustee to manage assets if the grantor becomes incapacitated. It is less costly to create than many other types of trusts. In community property states, the trusts inheritance is a separate asset of the beneficiary.

The trustee holds title to the property for another, called a beneficiary. Trusts are created for many reasons. Avoid probate court proceedings. Provide long-term management of property being held for the beneficiaries. Provide for certain tax exemptions and planning.

Charitable Remainder Trusts. Special Needs Trusts. Less Common Types of Trusts.You can name multiple trustees who can possess the gun, and it can be passed down to your successors even after your death without any transfer formalities. Trusts for Married Couples.

Types of Trusts for property owners.Number one is the Bare Trust. In this type of set-up, assets are handed over directly to the beneficiary when they turn 18 (or another specified age). This sort of Trust can even be used to maintain the confidentiality of the beneficiary.

Understand the various types of trusts available for asset protection and estate planning. Learn how each type serves a different purpose in safeguarding assets and providing for beneficiaries.

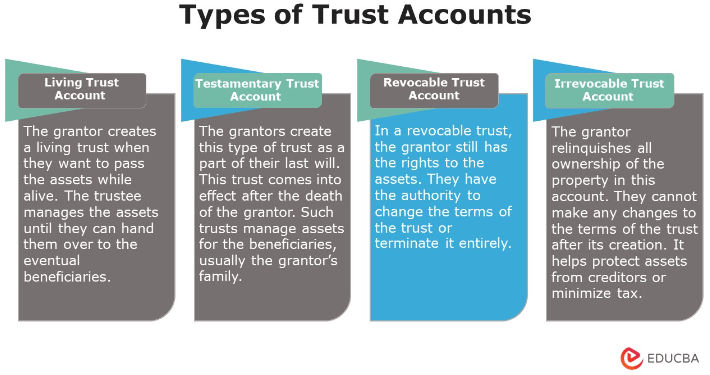

This particular example perfectly highlights why Types Of Trusts For Property Acquisition is so captivating.

Other Types of Trusts. Aside from revocable and irrevocable trusts, you can set up certain trust vehicles intended for specific purposes or financial goals. Here are some examples. Asset Protection Trusts.

Investment Analysis: Evaluating UK Property Trusts for Potential Returns. Key Takeaways. UK Property Trusts can be a solid addition to a diversified portfolio, offering a mix of stability and potential growth. Its vital to understand the types of property trusts and the specific markets they...

As we can see from the illustration, Types Of Trusts For Property Acquisition has many fascinating aspects to explore.

My client and his wife are the trustees of a trust that is looking to acquire a 999-year lease in a residential property. The trust does not currently own any other residential properties. What are the SDLT implications of the transaction? Will the 3% SDLT surcharge apply?

![Picture of Types of Trusts [INFOGRAPHIC]](https://www.johnsflaherty.com/i/1687962796435/x1168/uploads/content_files/images/types_of_trusts.png "Types of Trusts [INFOGRAPHIC]")

![View of Types of Trusts [INFOGRAPHIC]](https://www.johnsflaherty.com/i/1735499515000/x1168/uploads/content_files/images/Copy_of_types_of_trusts(2).jpg "Types of Trusts [INFOGRAPHIC]")